Article

Five things you didn’t know your credit card could do

Did you know there’s also a lot of hidden perks you could be getting with the right credit card?

Like most things, with great power comes great responsibility. And credit cards are no different. Used the right way, they can be your new financial BFF. But before you tap, swipe, and charge your way into a bold new financial future, it’s important to have a handle on the basics to avoid some of the downsides of living that plastic life.

What is a credit card?

In the most basic sense, a credit card is a piece of plastic that allows you to pay for things with borrowed money. It’s an agreement between you and a financial institution where you can opt to pay on credit rather than with actual money. In practice, it’s a little more involved than that. Your credit card comes with a limit—that is the amount of money you have to borrow against. And those charges? You’re going to pay interest on them if you carry a balance. But we’re getting ahead of ourselves.

Before you get swiping, make sure you know why. And how, so you can do it responsibly.

There are lots of reasons why having a credit card can make you into a financial superhero:

To build credit

Somewhere down the line, you will need a credit history. And a credit card—when used correctly—is one of the easiest ways to build credit. When the time comes to take out a car loan or get a mortgage, your financial institution will refer back to your credit history to see how reliable you are with borrowing money. So even if a credit card seems unnecessary, making frequent purchases with it and immediately paying it off will help you build a positive credit history, which will pay off in the future.

Flights, rentals, hotels, and online shopping

If you want to get on planes, trains, or automobiles, or to purchase the latest bobble from your favourite online retailer, you’re going to need a credit card. Ditto for booking a room in a hotel, booking concert tickets, and more.

Rewards

A lot of cards actually reward you for using them with things like cash back, travel points, or exclusive offers like concert tickets. As long as you’re managing your balance wisely, using your credit card frequently can help you treat yourself later.

Emergencies

Hopefully, it never happens, but every once in a while we all get stuck in emergencies where we don’t have cash on hand. And although you should never put something on your credit card if you don’t have the money to pay for it, your card might help you get out of a tough situation in the very short term – or at least until you can take stock of your situation and sit down with your financial expert to come up with a longer-term plan.

Now that you've decided to get a credit card, you have to ask yourself - which one should I apply for?

| No or Low Annual Fee Cards: These cards offer the convenience of having a credit card in your wallet without a high annual fee. Most low or no-annual-fee cards offer basic rewards but may not accumulate perks as quickly as a fee-based card. |

| Low-Interest Rate Cards: Many cards have interest rates upwards of 19.5%, but there are cards available with lower interest rates in exchange for a low annual fee. These cards often don’t accumulate rewards quickly, but if you find yourself carrying a balance on your card month over month, this can be a smart choice. |

| Rewards Cards: For every purchase you make on your card, you’ll accumulate a set number of reward points. Points can be redeemed for all sorts of different things, ranging from the latest gadgets and gift cards to concert tickets and experiences. |

| Student Cards: You guessed it! These cards are specifically meant for students who are just starting to build their credit. These often come with low or no fees and offer basic rewards. |

| Travel Rewards Cards: Similar to a rewards card, but focused on travel. Travel rewards cards feature points that can be redeemed for flights, hotels, and car rentals and often include insurance coverage for things like out-of-country medical, lost luggage, or changes to travel plans. |

| US Dollar Cards: These cards allow you to make purchases directly in US dollars. |

It’s a good idea to be honest with yourself about how you plan to use your card and what’s really important to you. For instance, if you’re keeping your card in case of emergencies only, a low or no annual fee card might make the most sense. If you find yourself travelling often, the protections and perks that come with a travel rewards card might provide you with the best value.

Once you have a better sense of your needs and habits, take the time to go online and do a little bit of research. Check out and compare different cards. Look at the features and benefits and what you need to apply. Some cards have a minimum income threshold to qualify or are designed specifically for students, so make sure you know what you’re getting yourself into.

Just because you want a credit card, doesn’t mean you can always get a credit card. Like any kind of credit, there is an application process to complete before you can start spending.

Don’t apply for every offer: Each time you apply for a credit card there will be an inquiry made on your credit history. Lots of inquiries over a short period of time can impact your credit score and lots of open, available cards can hurt your chances to qualify for more credit in the future.

So, you have your credit card. Now what? While using your card is pretty straightforward, there are a couple of important things to know about managing your card.

First, not every purchase on a credit card is created equal. While most of us tend to think of credit card purchases as tapping or swiping your card in a store or inputting your information online, you can also use your credit card to get cash or to make cash-like transactions. This is called a cash advance.

Taking a cash advance might sound like a good idea, but this can be a costly way to access cash in the long run. Cash advances often charge a small fee to initiate and almost always charge a higher rate of interest than regular purchases. The other thing to keep in mind is how interest accumulates. With regular purchases, you have a grace period (usually 21 days or more) before interest begins to accumulate on the money you owe. When you take a cash advance, interest starts to accumulate right away and will continue to accrue until the whole amount of the advance is paid off in full.

You can also expect to get a monthly statement whether you use your card or not. Statements provide a detailed snapshot for a set period of time and outline your purchases, how much you owe, the minimum payment due, and when you need to make a payment. Statements are monthly, but may not run from the first day of the month to the last.

When you get your statement, be sure to review it carefully. If something doesn’t make sense on your statement, or if there is something you don’t recognize, don’t be afraid to speak up and ask your card provider for more details.

| DO | DON'T |

|

|

Be aware of your terms and conditions: If an offer seems too good to be true, it probably is. And the same goes for credit cards. Be cautious when it comes to 0% offers in exchange for making a big purchase and be sure that you understand the terms and conditions before signing up. Zero interest doesn’t mean forever and some credit cards can charge very high rates once their introductory offers have expired.

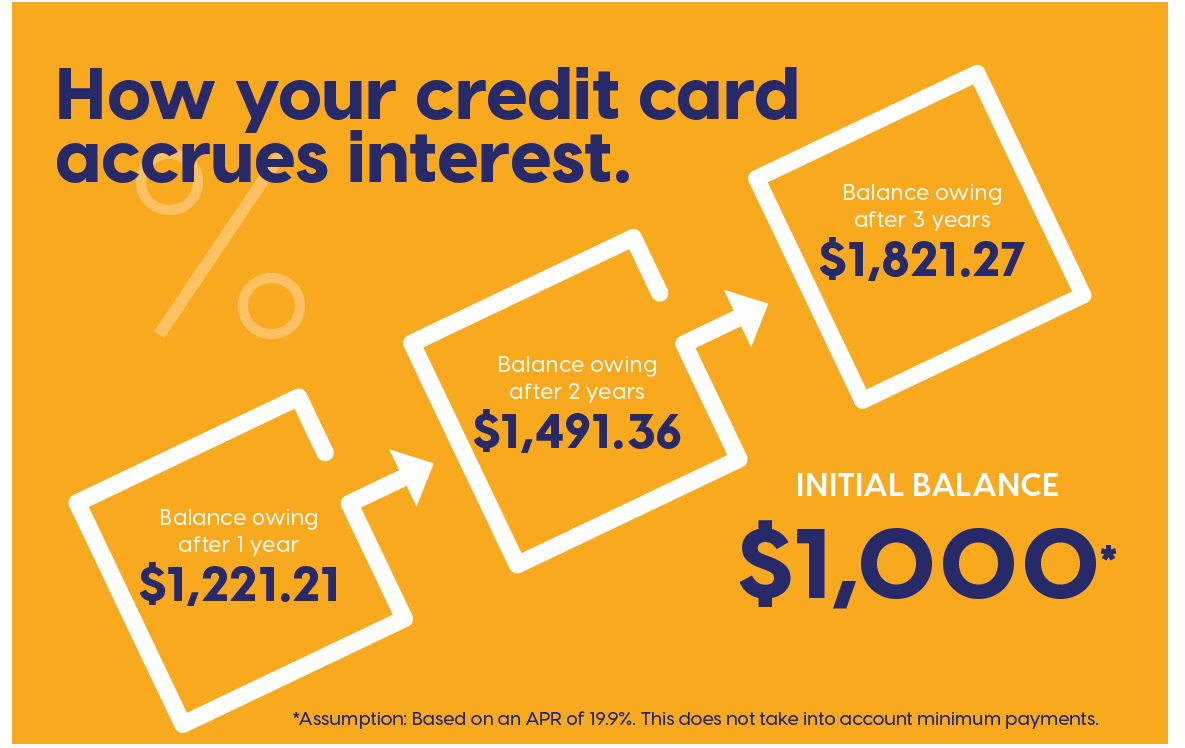

Every credit card has an interest rate. When you make a purchase with your credit card, your grace period for that transaction starts. This means that you have around 21-25 days (each credit card provider is different) to pay off that transaction before interest charges kick in. If you keep an unpaid balance on your credit card, interest will keep adding up month by month. But if you pay off the full balance on time, you’ll never have to pay interest! And remember, only making the minimum payment required each month still means you get charged interest on the full balance.

Credit cards have a lot of great security features, but knowing how to protect your card information is probably the biggest thing you can do to keep yourself from fraud. Here are a few easy tips that can help.

| APR: This is short for Annual Percentage Rate. APR is the rate charged to the amount borrowed on your credit card, expressed as a percentage. (See Interest Rate definition.) |

| ANNUAL FEE: A yearly fee that is charged for having certain credit cards in your wallet. Not all credit cards have annual fees. The fee can range in price and typically includes access to other perks, points, or benefits above and beyond what you get with a standard, no-fee card. |

| BALANCE: This is how much money you owe on your credit card. |

| CREDIT LIMIT: The maximum dollar amount you can spend on your credit card. |

| GRACE PERIOD: Typically, when you make a purchase on your credit card, interest doesn’t begin to accumulate immediately. Instead, you get a grace period (usually a minimum of 21 days) to make payments before you are charged interest. If you pay off the full amount owing on your card before the end of your grace period, you will not be charged interest. |

| INTEREST RATE: This is the percentage of interest that is charged on any balance owing on your card after the grace period is up. Interest is calculated daily and charged to your card monthly. Interest rates can vary from card to card. |

| MINIMUM PAYMENT: This is the smallest dollar amount that you can pay each month to keep your credit card account in good standing. |

| STATEMENT: Your credit card statement is a detailed list showing all of your transactions during your billing cycle, along with your balance owing (as of your statement date), your minimum payment, and when your payment is due. |

If you'd like to download this guide, please click here. If you'd like to learn more or discuss your options, please reach out to your local credit union.