Article

Consider this before buying your first home

A few things you should know about Canada's First-Time Home Buyer Incentive and what it means for you.

Maybe you live in the best apartment ever with a great landlord and don’t want to change a thing. Or maybe you’ve looked at how much rent money you’ve been putting in somebody else’s pocket and have decided you’re ready to look at your options. Either way, we can help.

So, you think you might be interested, but where do you start? Condo or house? City or burbs? Fixed-rate or variable mortgage? Open or closed? What’s an amortization period, anyway?! We’re here to help you get the answers to all your questions. Buying your first home is an incredibly exciting time, and with the right partner helping you, it can be relatively painless, too.

A great place to start is with this guide. From helping you understand how much buying a home really costs, to walking you through the entire process right up to moving day, we’ll cover all the stages of homeownership. This is the single biggest investment of your life! We’ll help you do it right.

Thinking about homebuying? Try our mortgage payment calculator to help you find the payment for your budget.

Find Out MoreCAN I AFFORD TO BUY A HOME?

The actual cost of buying a home goes beyond the purchase price and your mortgage payment. Aside from your scheduled mortgage payments, there are several upfront costs involved in the process like closing costs, inspections, appraisals, taxes, maintenance, legal fees, and a down payment. These costs should all be factored into your initial budget.

CAN I AFFORD NOT TO?

Think of homeownership as an investment in your future. If you have a stable, secure income, and are ready to start building equity, homeownership is definitely something you should investigate further.

AM I READY FOR THE RESPONSIBILITY?

When you own your own home, you can do whatever you want—so go ahead and paint that powder room lime green! On the other hand, you’ll be on your own when it comes to fixing a clogged sink or if your washing machine bites the dust. There’s no sugar-coating the fact that owning a home can be a lot of work. At the same time, there’s a great reward in taking a house and really making it your home.

WHAT EXACTLY DO I WANT/NEED IN A HOME?

Are you looking for a home with a yard big enough to plant seven different varieties of kale? Or is downtown condo living more your style? What kind of neighbourhood do you want to live in? Are schools or public transit a consideration? Do you want your home to be move-in ready, or are you willing to roll-up your sleeves and get your hands dirty? Take the time to think about everything you’re looking for in a home—from size, to location, to amenities—and write it all down. Take your list with you when you start looking at homes with your real estate agent. It’ll help keep you on track.

DOLLARS AND SENSE:

Your monthly housing costs (including your mortgage payment, property taxes, and heating expenses) ideally should not be more than 35% of your gross monthly income. Your entire monthly debt load (including housing costs, plus all other debt payments like student loans, car loans/leases, credit card payments, line of credit payments, etc.) ideally should not be more than 42% of your gross monthly income.

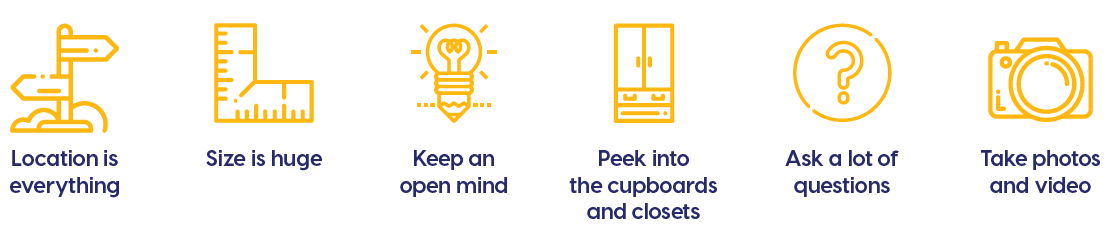

LOCATION IS EVERYTHING. While you can always add on an extra room or even a floor to your home, you can’t exactly change your neighbourhood. Think about the things that are important to you—a big yard vs low-maintenance, rural vs urban, nearby amenities, transportation, etc. Keep these things in mind when you’re exploring different neighbourhoods.

SIZE IS HUGE. There’s such a thing as not having enough room. But it’s also possible to have too much house. Think about what you need now, but also consider what you may need in the future. Home office? Kids’ rooms? Yard for pets? A finished basement? Make a list of the things you can’t live without and take it with you when you look.

KEEP AN OPEN MIND. Look past the surface. A coat of paint, some new light fixtures, and different furniture can go a long way. The same goes for a house that has been professionally staged: Don’t fall for it! Look beyond the presentation and focus on the structural features—that’s really what you’re buying.

PEEK INTO THE CUPBOARDS AND CLOSETS. Look up at the ceiling and down at the foundation. Flush the toilets. Turn on the showers. Check out every nook and cranny. If there are unexplained water marks on floors or ceilings, or hasty repair jobs, make note and have your home inspector take a closer look.

ASK A LOT OF QUESTIONS. The only question you will regret is the one you didn’t ask. Ask questions as they pop into your head. How long did the previous owners live in the house? How old are the appliances? What are the neighbours like? When was the last time the roof was re-shingled? What is the average monthly heating cost? What is the annual property tax amount? The real estate agent might not know all the answers, but they’re questions worth asking.

TAKE PHOTOS AND VIDEOS. You think you’ll remember the details, but you won’t. When you get home, print out the photos and make notes on them. List your likes/dislikes and the pros/cons for each. This is a good way to process what you’ve seen and will also come in handy when you’ve narrowed your search down to a couple of possibilities and want to look at them side-by-side.

Getting approved for a mortgage to purchase your first home is a big deal. It’s also a big financial commitment and an emotional decision. The first step to finding your way through the mortgage process is getting a financial institution’s pre-approval on a mortgage amount. This will give you a frame of reference for what you can afford.

It all starts with a pre-approval meeting with a trusted financial institution. We recommend taking documents like ID, proof of address, proof of employment, proof

of income, social insurance number, account balances, etc. (for a full checklist of documents to bring, refer to the Mortgage Document Checklist at the end of this guide) with you to this meeting. This will give the lender information about your overall financial situation, and will help them make recommendations that work for your individual needs.

Your down payment amount will be a big factor in determining your pre-approval amount. Down payments generally start from 5% of the purchase price. The more you can save toward your down payment, the more you’ll save in the long run—we’re talking thousands of dollars.

A mortgage is essentially a secured loan used to purchase a property. In order to guarantee the repayment of the loan, the property is used as security. This means your lender can take ownership of the property if payments are not made on time.

PRINCIPAL VS INTEREST

Interest on a loan is essentially the “cost” of borrowing money for a set period of time. The borrower (you) pays interest to the lender (a financial institution like a credit union) in installments, along with payments on the principal loan amount.

Principal refers to the amount of money borrowed.

Together, interest and principal make up your house payments. Our Mortgage Calculator will help you find the payment that fits in your budget.

A CONVENTIONAL MORTGAGE is a mortgage that is no more than 80% of the purchase price or the appraised value of the home (whichever is less). The benefit of a conventional mortgage is, if you can save at least 20% of your purchase price, you will save the added expense of having to pay for default insurance, which is required with a high ratio mortgage.

A HIGH RATIO MORTGAGE is a loan over 80% (up to 95%) of the purchase price, or appraised value of the home (whichever is less). This mortgage option requires the value of the mortgage to be insured against default by an approved insurer, like the Canada Mortgage and Housing Corporation (CMHC), a federal government corporation, or a private insurer, like Sagen™.

You will have to pay a premium for this insurance, which can be paid upfront or included in the principal portion of your mortgage. The benefit of a high-ratio mortgage is if you are unable to save a 20% down payment, you can still potentially purchase a home.

There are many different kinds of mortgages. Each feature different benefits or risks by offering different interest rates, flexibility in payment schedules, and options for renegotiation. We will discuss these options with you and answer any questions you may have about choosing the right mortgage for you.

The chart below outlines the features and benefits of your mortgage options. A credit union Mortgage Specialist can help you determine which options are best suited for your needs based on a full assessment of your current financial situation and future goals.

| TYPE | FEATURE | BENEFIT |

|---|---|---|

| Fixed Rate Mortgage | Interest rate locked for the term of the mortgage. | Security and peace of mind. The interest rate will not increase over the term of the mortgage. Regularly scheduled payments do not change. If the interest rate goes down, you risk paying more interest over the term of your mortgage. Your mortgage 'term' is the fixed period of time that you've committed to a specific interest rate and conditions with a lender. Common terms range from 1–5 years. At the end of the term, you will need to renegotiate a new term. |

| Variable Rate Mortgage | Interest rate changes with the market. | Low interest rate. If interest rates go down, you could pay off your mortgage faster. If interest rates go up, you risk paying more interest over the term of the mortgage. With an uncapped (adjustable rate) mortgage, your monthly payment will fluctuate with prime rate. With a capped (variable rate) mortgage, your monthly payment doesn’t change when prime rate changes. The only exception is when rates soar, you’re not paying all the interest. The payment generally rises to cover the interest due. With a capped mortgage, the rate will fluctuate depending on the market, but will never exceed a maximum rate established when you originally take out your mortgage. |

| Open Mortgage | Pay off your mortgage at any time without penalty. | Flexibility. Short-term option. An open mortgage offers flexibility to pay off your mortgage in part, or in full, at any time without penalty. It also allows you to renegotiate your term at any time. This option comes at a higher interest rate and therefore is usually only considered for the short-term. This could be a great option if you plan to sell again in the short-term. |

| Closed Mortgage | Cannot pay off your mortgage without penalty. | Lower interest rate. Long-term option. A closed mortgage does not offer the flexibility to pay off or renegotiate your mortgage at any time. However, you do receive a lower interest rate reducing the overall interest cost of your mortgage over the term. |

| Mortgage Secured Line of Credit/ Home Equity Line of Credit | Use the equity in your home to secure up to 80% of the purchase price of value of your home. | Low interest rate. Flexibility. This is a great option for anyone who is confident in their ability to manage the line of credit responsibly and anyone who can ensure that a payment schedule will be put in place to manage the funds. Funds can be used for any reasonable purchase, such as home renovations, a new car, etc. |

| Collateral Mortgage/ Collateral Charge Mortgage | Register your mortgage for up to 125% of the value of your home at closing. | Access to more funds after closing without extra costs. A collateral charge mortgage generally makes it easier to refinance by avoiding legal costs. It doesn’t allow a lender to change a fixed rate or the discount on a variable-rate mortgage. However, it does allow the lender to change the rate if you ask for more money later or if you have a line of credit portion with a floating rate. |

This mortgage checklist will help you prepare for your meeting with your financial expert. And here is your home buying checklist to help you understand additional costs of purchasing a home.

To download this guide for future reference, click here.

If you'd like to learn more or discuss your options, please reach out to your local credit union.